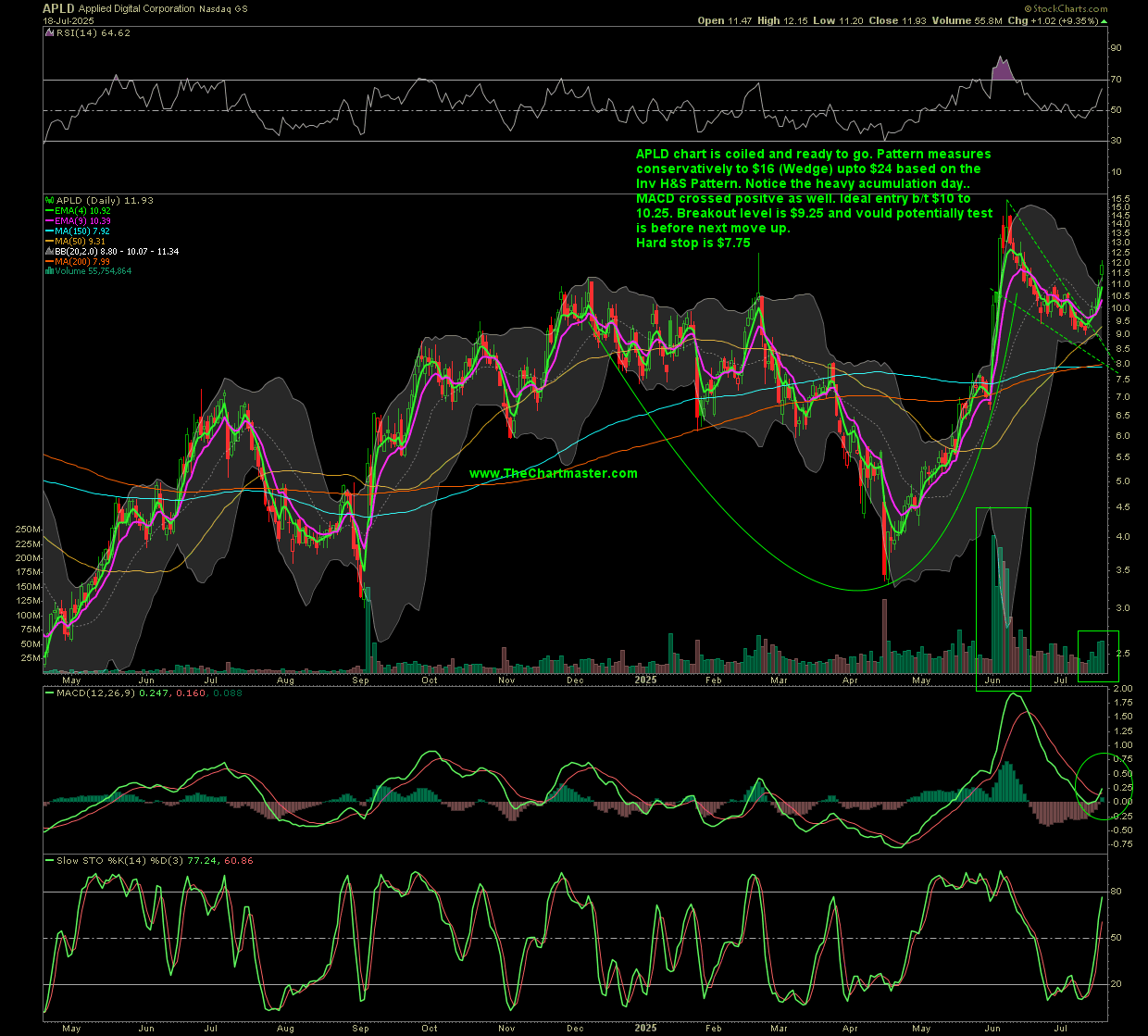

Thesis Overview

Applied Digital is strategically pivoting to become a leading provider of next‑generation infrastructure, capitalizing on explosive AI and HPC demand. The standout catalyst is its recently secured flagship partnership with CoreWeave, securing a long‑term lease and stable cash flows. Despite the current unprofitable status and high leverage, the firm’s trajectory toward becoming a data‑center REIT is promising and well‑supported by strong demand anchors.

✅ CoreWeave Win: A Transformational Deal

- $7 billion, 15‑year lease commitment to host CoreWeave’s AI/HPC infrastructure at Ellendale, ND (250 MW on initial build, with an option for +150 MW) Sherwood News+15Applied Digital Corporation+15Simply Wall St+15.

- Revenue anchor: this deal underpins long-term revenue, offering growth visibility through 2039.

- Strategic positioning: establishes Applied Digital as a prime infrastructure and REIT contender in the AI data‑center space, with potential for additional enterprise tenant deals Business Insider.

📈 Recent Earnings & Financial Highlights (Q1 CY2025)

(Source: StockStory review of Q1 CY2025) StockStory+1Finviz+1

- Revenue: $52.9 M (↑22.1% YoY), though below Wall Street estimates (~$64.5 M).

- Adjusted EPS: –$0.08 (beats estimate of –$0.10).

- Adjusted EBITDA: $10.0 M, with 18.9% margin (vs. est. $16.9 M).

- Operating margin: –35.8% (improvement from –73.2% YoY).

- Free Cash Flow: –$251.6 M, deepening from –$2.3 M YoY – reflecting aggressive campus investment.

- Guidance: CEO noted technical infrastructure hurdles in cloud transitioning, but reiterated confidence in future data‑center revenue expansion and improved margins.

🎙️ Earnings Call Insights

- Management reiterated that the CoreWeave leases “solidify” APLD’s position in AI/HPC infrastructure Business Insider+5StockStory+5Finviz+5Sherwood News+15Reuters+15GlobeNewswire+15.

- Emphasis placed on balancing growth and interest burden, with ongoing capital raises (e.g., SMBC $375 M, $150 M convertible preferred, Macquarie $5 B equity line) to mitigate funding risk Applied Digital Corporation+1Lowenstein Sandler+1.

- Operational focus includes boosting campus buildouts (100 MW by Q4 2025, next buildings in 2026–27) and scaling cloud services to complement infrastructure leasing.

⚖️ Risk / Reward Summary

| Catalysts (Upside) | Risks (Downside) |

|---|---|

| Stable, long‑term CoreWeave revenue | Elevated debt and ongoing capex needs |

| AI/HPC demand tailwinds & potential new tenants | Continued free cash flow deficits |

| Transition toward REIT structure – potential valuation upside | Execution risk on construction timelines and cost control |

| Improving operating margins as scale increases | Cloud services segment underperformance |

💡 Valuation & Target Price

- Market cap ~$2 B; trading ~19× forward EV/EBITDA StockStoryBusiness Insider+1Reuters+1 — rich for an unprofitable operator.

- Street forecasts envision break-even EPS by 2026–27 and accelerating free cash flow as Ellendale ramps.

- Given the long-term lease, AI momentum, and REIT narrative, investors estimating conservative growth may price fair value between $15–$20, while bears (concerned by leverage) see downside near $10.

🔍 Final Take

Applied Digital checks the boxes as a speculative AI‑infra play with a monumental CoreWeave partnership anchoring its future. While financials remain strained given high debt and negative cash flow, the company is on a clear upgrade path—building valuable data-center assets backed by long-term tenant commitments. Positive earnings, margin progress, and successful campus execution will likely drive investor enthusiasm. For risk-tolerant investors looking to play the AI infrastructure boom, APLD presents a compelling, albeit volatile, asymmetric opportunity.

Leave a Reply